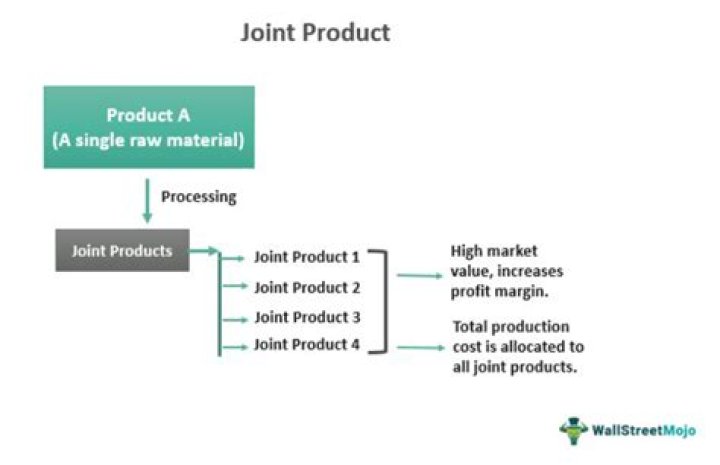

Joint products are two or more products that are generated within a single production process; they cannot be produced separately and incur undifferentiated joint costs. Examples of join products include: Milk – butter, cream, cheese. Crude oil – fuel, gas, kerosene.

What do u mean by joint product?

In Economics, joint product is a product that results jointly with other products from processing a common input; this common process is also called joint production. A joint product can be the output of a process with fixed or variable proportions.

What is joint product and by-product?

A joint product is manufactured consciously and simultaneously along with the main product, whereas the by-product is simply an incidental result of the manufacturing of the main product.

What are joint products give two examples?

Few examples of joint products are:

- Processing of crude oil to obtain gasoline, diesel, asphalt, jet fuel and lubricants etc.

- Production of butter, cheese and cream from milk.

- Different grades of wood obtained from a same kind of tree.

What is joint cost example?

A joint cost is a kind of common cost that occurs after a raw product, such as a sunflower crop, undergoes two separate production processes. For example, the cost of fertilizing and harvesting sunflowers qualifies as a common cost. Another example of joint costing is feeding both sheep and cattle.

What are the features of joint products?

Following are the characteristics of joint products:

- The value of all the joint products is more or less the same.

- Such products don’t necessarily require processing after a point of separation.

- Such products need simultaneous standard processing.

- The raw material or materials they use are the same.

What are the features of joint product?

What will justify the treatment of a product as joint product?

Justification of the treatment of joint product as by-product: A joint product is normally treated as a by-product if its sales value is relatively minor compared to other joint products.

What is joint cost process?

In accounting, a joint cost is a cost incurred in a joint process. Joint costs may include direct material, direct labor, and overhead costs incurred during a joint production process. A joint process is a production process in which one input yields multiple outputs.

What are joint products and joint costs?

A joint cost is a cost that benefits more than one product, while a by-product is a product that is a minor result of a production process and which has minor sales. Besides the split-off point, there may also be one or more by-products.

What are the objectives of joint cost analysis?

Objectives of Joint Cost Analysis 1. Correct collection, compilation and classification of process costs. 2. The profit or loss of joint products manufacture is determined.

How do we allocate joint product cost?

How to Allocate Joint Costs

- Allocate based on sales value. Add up all production costs through the split-off point, then determine the sales value of all joint products as of the same split-off point, and then assign the costs based on the sales values.

- Allocate based on gross margin.

Why do we allocate joint costs?

In cost accounting, joint costs are production costs incurred in creating two (or more) products. Those costs are attached to inventory and expensed when the product is sold. So you need joint costs to calculate inventory values and the cost of goods sold.

How Nfps should allocate joint costs?

ASC Paragraph 958-720-50-2, Not-for-Profit Entities—Other Expenses—Disclosure—Accounting for Costs of Activities That Include Fundraising, requires that an NFP that allocates joint costs disclose the types of activities for which joint costs have been incurred, a statement that such costs have been allocated, the total …

What is joint cost allocation?

Joint Cost Allocation To use this method, simply divide the total production cost by the appropriate measure of output volume to yield the cost per unit of output. One type of monetary measure of joint cost allocation is the sales value method. Then divide them into proportions of sales value that add up to 100%.

What is the best joint cost allocation method?

The splitoff method in cost accounting Allocating joint costs using sales value at splitoff may be the most effective method for planning and budgeting for joint costs. Here are several reasons why: No information on separable costs is required. The sales value at splitoff may be the best comparison of the products.

What are the 3 methods that joint costs can be allocated?

Three methods of allocating joint product costs are the physical units method, the market value method, and the net realizable method. The constant gross margin percentage method is also used to allocate joint cost.

How do you allocate joint costs?

Few examples of joint products are: Processing of crude oil to obtain gasoline, diesel, asphalt, jet fuel and lubricants etc. Production of butter, cheese and cream from milk. Different grades of wood obtained from a same kind of tree.

Joint Product. By-Product. Meaning. When the production of two or more products of similar value, are made together with same input and process, is called joint product. The term by-product means a product which is incidentally produced, during the processing operation of another product.

What is a joint product in process costing?

Joint products are two or more products separated in the course of processing, each having a sufficiently high saleable value to merit recognition as a main product. Joint products include products produced as a result of the oil-refining process, for example, petrol and paraffin.

What is joint and product in cost accounting?

A joint cost is a cost that benefits more than one product, while a by-product is a product that is a minor result of a production process and which has minor sales. The point at which the business can determine the final product is called the split-off point.

What is the difference between common cost and joint cost?

Difference between Joint Cost and Common Cost: Common costs are not the result of any manufacturing compulsion or the use of any single raw material. The incurrence of common costs are influenced by management decisions, But joint costs are influenced by common production process and use of common raw materials.

How do you calculate joint cost?

One of the simplest methods to apportion joint cost is the average unit cost method. Here, the average cost per unit is calculated by simply dividing the total cost of all the joint products incurred before their splitting-off, by the total of the number of units produced all together.

What’s the difference between a by product and a joint product?

The major points of difference between joint product and by-product are given below: A Joint product is one which is manufactured ancillary to the production of the main production, hence the purpose is intentional. However, a by-product is purely an unintentional consequence of the production of the main product.

What are joint products and how to invoice them?

Joint products – What are joint products? Joint products are two or more products that are generated within a single production process; they cannot be produced separately and incur undifferentiated joint costs. Take charge of your invoicing and accounting with Debitoor invoicing software. Try Debitoor free for 7 days.

How are joint costs divided among joint products?

Under this method the joint costs are apportioned among the joint products in the ratio of physical units of output produced at the point of separation. For example, the physical base like raw material weight in physical quantity is used as the base for apportioning the joint costs.

How are net sales values used in joint products?

From these values of joint products, the further processing costs are deducted and net sales value at the point of separation is ascertained. These net sales values are used as the basis for apportioning the joint costs to individual products. It is a good method for product pricing but not for planning and control.